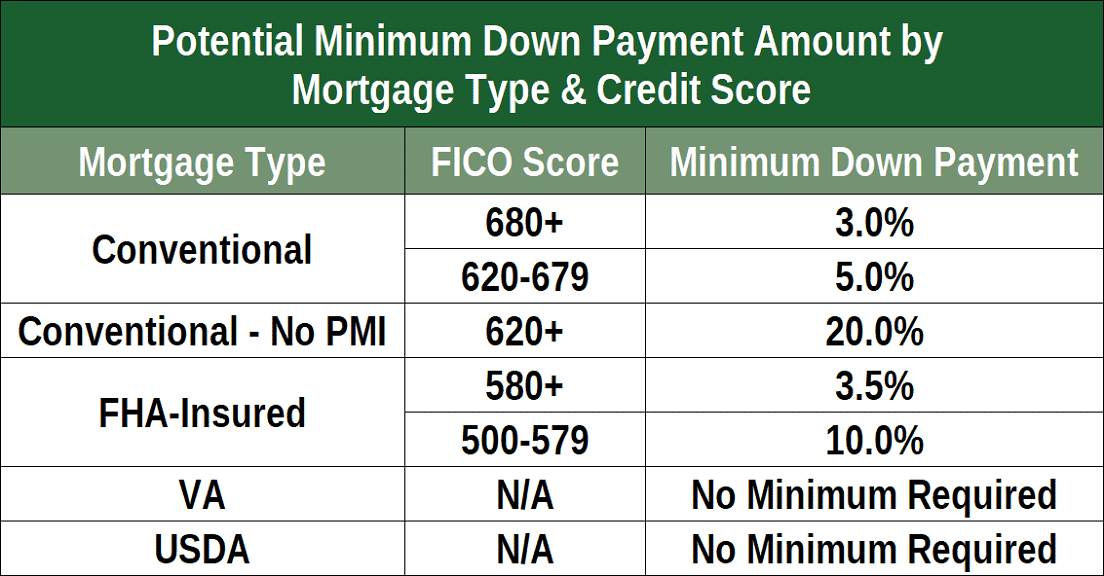

# Credit Score Requirements for a Kentucky Mortgage Loan in 2025 – And How to Improve Yours Fast **Meta Title:** Credit Score Requirements for a Kentucky Mortgage Loan | Joel Lobb **Meta Description:** Find out the minimum credit scores needed for FHA, VA, USDA, KHC, and Fannie Mae loans in Kentucky in 2025 — plus proven tips to boost your score before you buy. **URL Slug:** credit-score-requirements-kentucky-mortgage-loan **Primary Keyword:** credit score requirements Kentucky mortgage **Secondary Keywords:** how to improve credit score Kentucky home buyer, Kentucky FHA credit score, KHC credit score requirements, minimum credit score Kentucky mortgage, first time home buyer credit score Kentucky --- If you're planning to buy a home in Kentucky and wondering whether your credit score is good enough — you're asking exactly the right question. Your credit score is one of the most important factors in getting approved for a mortgage, and it also directly affects your interest rate and monthly payment. The good news? You don't need perfect credit to buy a home in Kentucky. Whether you're a first-time homebuyer in Louisville, Lexington, Bowling Green, or anywhere in the Bluegrass State, there are loan programs available with flexible credit requirements — including options with zero down payment. In this guide, Kentucky Mortgage Loan Officer **Joel Lobb** (NMLS #57916) breaks down exactly what credit scores you need for each major loan program in Kentucky, explains what goes into your FICO score, and gives you step-by-step tips to raise your score quickly so you can get approved and into a home sooner. --- ## Minimum Credit Score Requirements by Loan Type in Kentucky (2025) Before you start house hunting, you need to know your number. Here's what lenders typically look for on each major Kentucky mortgage program: ### FHA Loans – Kentucky's Most Popular First-Time Buyer Option The **Federal Housing Administration (FHA) loan** is the go-to program for Kentucky first-time homebuyers with less-than-perfect credit. Here's how the credit score tiers work: - **580+ credit score** → Eligible for the minimum **3.5% down payment** - **500–579 credit score** → May still qualify, but requires a **10% down payment** - **Below 500** → Not eligible for FHA financing FHA loans are especially popular in Kentucky because they allow gift funds for the down payment, accept higher debt-to-income ratios, and are available statewide — in both cities and rural areas. ### VA Loans – Zero Down for Kentucky Veterans If you are a veteran, active-duty military, or surviving spouse, a **VA loan** offers the best terms available — including no down payment and no monthly mortgage insurance. The VA does not set a minimum credit score, but most Kentucky lenders require at least a **580–620 FICO score**. Some lenders may work with scores as low as **500** with strong compensating factors such as low debt ratios or significant residual income. ### USDA / Rural Development Loans – Zero Down in Eligible Kentucky Areas The **USDA Rural Development loan** is one of the best-kept secrets in Kentucky mortgage lending. It requires **zero down payment** and is available to low-to-moderate income buyers in USDA-eligible areas — which covers a large portion of Kentucky, including many suburban communities outside Louisville and Lexington. USDA loans typically require a **640+ credit score** for automated underwriting approval. Scores below 640 may require manual underwriting with additional documentation. ### KHC Loans – Kentucky Housing Corporation Down Payment Assistance **Kentucky Housing Corporation (KHC)** loans are specifically designed for Kentucky first-time homebuyers and offer below-market interest rates plus down payment assistance programs. - **Minimum credit score: 620** for most KHC programs - KHC down payment assistance is available as a loan or grant — currently up to several thousand dollars — to help with your down payment and closing costs - KHC programs can be paired with FHA, VA, USDA, or Conventional financing ### Conventional / Fannie Mae Loans Conventional loans backed by **Fannie Mae** offer excellent terms for buyers with stronger credit: - **Minimum credit score: 620** for Conventional loan approval - **Score of 740+** typically qualifies you for the best interest rates available - Fannie Mae's **HomeReady** program allows as little as **3% down** for income-eligible buyers --- ## Quick Reference: Kentucky Mortgage Credit Score Chart | Loan Program | Minimum Credit Score | Down Payment | |---|---|---| | FHA | 580 (500 with 10% down) | 3.5% | | VA | 580–620 (varies by lender) | 0% | | USDA Rural Development | 640 | 0% | | KHC (Kentucky Housing) | 620 | Down Payment Assistance Available | | Fannie Mae Conventional | 620 | 3–5% | | Fannie Mae HomeReady | 620 | 3% | --- ## Why Your Credit Score Matters Beyond Just Getting Approved Your credit score doesn't just determine whether you get approved — it determines the **interest rate you pay for the life of your loan**. Even a 20-point difference in your score can mean hundreds of dollars per year in interest. For example, on a $200,000 Kentucky mortgage: - A borrower with a **760 score** might qualify for a rate of 6.5%, resulting in a payment of approximately **$1,264/month** - A borrower with a **640 score** might be offered 7.5%, putting the payment at approximately **$1,398/month** That's over **$1,600 per year** in extra interest — or more than **$48,000 over the life of a 30-year loan** — simply due to a 120-point difference in credit scores. **This is why taking even 60–90 days to improve your score before applying can be one of the most financially impactful decisions you make.** --- ## What Makes Up Your FICO Credit Score? Understanding the five components of your FICO score is the first step to improving it. Here's how each factor is weighted: 1. **Payment History (35%)** — The most important factor. Do you pay your bills on time? Even one 30-day late payment can drop your score significantly. 2. **Amounts Owed / Credit Utilization (30%)** — How much of your available credit are you using? Keeping balances below 30% of your credit limit (and ideally below 10%) has a major positive impact. 3. **Length of Credit History (15%)** — How long have your accounts been open? Older accounts with good history help your score. Avoid closing old credit cards before applying for a mortgage. 4. **Credit Mix (10%)** — Having a mix of account types (credit cards, auto loans, student loans) shows lenders you can manage different types of debt responsibly. 5. **New Credit / Hard Inquiries (10%)** — Applying for multiple new credit accounts in a short period can temporarily lower your score. Avoid opening new credit cards or financing furniture in the months before applying for a mortgage. --- ## 10 Proven Ways to Improve Your Credit Score Before Buying a Kentucky Home If your score isn't quite where it needs to be, don't get discouraged. Many Kentucky homebuyers have raised their scores by 20 to 100+ points in just 3 to 6 months by following these steps: ### 1. Pull Your Free Credit Reports and Dispute Any Errors Get your free reports from all three bureaus — **Equifax, Experian, and TransUnion** — at [AnnualCreditReport.com](https://www.annualcreditreport.com). Look for: - Accounts that don't belong to you - Late payments reported incorrectly - Duplicate collection accounts - Accounts listed as open that you've paid off Disputing and removing errors is one of the fastest ways to raise your score, sometimes resulting in a 20–50 point increase. ### 2. Pay Down Credit Card Balances Your **credit utilization ratio** — how much of your available credit you're using — accounts for 30% of your score. If you have a credit card with a $5,000 limit and a $4,000 balance, your utilization is 80%, which severely hurts your score. Goal: Get each card's utilization **below 30%**, ideally below 10%. ### 3. Never Miss a Payment — Set Up Autopay Since payment history is 35% of your score, a single missed payment can cost you 50–100 points. Set up autopay for at least the minimum payment on all accounts so you never accidentally miss a due date. ### 4. Don't Close Old Credit Card Accounts It might seem smart to close cards you don't use, but doing so shortens your credit history and increases your utilization ratio. Both hurt your score. Keep old accounts open — just put a small recurring charge on them to keep them active. ### 5. Become an Authorized User on Someone Else's Account If a family member or trusted friend has a credit card with a long history and low utilization, ask them to add you as an **authorized user**. Their positive history can appear on your credit report and boost your score — even if you never use the card. ### 6. Address Collection Accounts Strategically Having a collection account on your report doesn't always mean you need to pay it off to qualify for a mortgage — it depends on the loan type. However, **medical collections are now treated differently** by most mortgage underwriting systems and may have less impact on your qualifying score. Talk to your loan officer before paying off collections, as it can sometimes temporarily lower your score. ### 7. Avoid Applying for New Credit Before Your Mortgage Every time you apply for a credit card, car loan, or store financing, the lender does a **hard inquiry** on your credit, which can drop your score by 5–10 points temporarily. Avoid new credit applications for at least 6 months before applying for a mortgage. ### 8. Use a Secured Credit Card to Build Credit If you have limited credit history or are rebuilding after problems, a **secured credit card** (where you deposit money as collateral) can be a powerful tool. Use it for small purchases and pay it off in full each month. After 6–12 months of on-time payments, you'll see your score climb. ### 9. Keep Accounts Open During the Mortgage Process Once you've been pre-approved and are under contract on a home, do not open or close any accounts. Your lender will pull your credit again before closing, and changes to your profile can delay or derail your approval. ### 10. Ask for a Rapid Rescore Through Your Lender If you've paid down a balance or had an error removed, ask your Kentucky mortgage loan officer about a **Rapid Rescore**. This is a service that can update your credit report and recalculate your score within 3–5 business days — much faster than waiting for the bureaus to update naturally. This can be a game-changer if you're close to a qualifying score threshold. --- ## Kentucky-Specific Credit Tips: What I've Seen Working With 1,300+ Kentucky Families After helping more than 1,300 Kentucky families buy or refinance their homes over 20+ years, here's what I've found works best for buyers in our state: **Take advantage of KHC down payment assistance.** Kentucky Housing Corporation programs help buyers who are close to qualifying get across the finish line. If your score is at or above 620, we may be able to pair a KHC down payment grant with an FHA or Conventional loan and get you into a home with very little out of pocket. **Don't assume you need to wait.** Many buyers come to me thinking they need a year or more to fix their credit. In many cases, two to three targeted moves — disputing an error, paying down one card, and removing an old collection — can get a buyer from a 580 to a 620 in 60 days. **Get pre-qualified before you're "ready."** I offer free same-day pre-qualifications. Even if your score isn't where it needs to be yet, I can create a personalized credit improvement roadmap specifically for your situation. No cost, no pressure, no obligation. --- ## Frequently Asked Questions: Credit Scores and Kentucky Mortgage Loans **What is the minimum credit score to buy a house in Kentucky?** It depends on the loan program. FHA loans allow scores as low as 500 (with 10% down) or 580 (with 3.5% down). VA and USDA loans require 580–640 depending on the lender. KHC and Conventional loans typically require a 620 minimum. **Can I get a Kentucky mortgage with a 580 credit score?** Yes. A 580 FICO score qualifies you for an FHA loan with 3.5% down. You may also qualify for a VA loan (if eligible) with a 580 score through certain lenders. KHC and USDA loans typically require a 620 minimum. **How long does it take to improve a credit score?** Small improvements — like paying down a credit card balance or having an error removed — can show results in 30 to 60 days. More significant rebuilding after bankruptcy or foreclosure can take 1 to 3 years. **Does checking my own credit score hurt it?** No. When you check your own credit (a "soft inquiry"), it does not affect your score. Only "hard inquiries" from lenders when you apply for credit can temporarily lower your score. **What credit score do I need for a USDA loan in Kentucky?** Most USDA lenders in Kentucky require a **640 credit score** for automated underwriting approval. Scores between 580 and 639 may be considered through manual underwriting with compensating factors. **What credit score do I need for a KHC down payment assistance loan?** KHC requires a minimum **620 credit score** for most of its loan programs and down payment assistance options. --- ## Ready to Find Out Where You Stand? Get a Free Same-Day Pre-Qualification You don't have to figure this out alone. Whether your credit is strong, a work in progress, or you're not sure where you stand — I'm here to help. I've worked with Kentucky buyers across the credit spectrum and can tell you exactly what you qualify for today and what steps will get you to your goal faster. **Joel Lobb — Kentucky Mortgage Loan Officer** 📞 **Call or Text:** [502-905-3708](tel:5029053708) 📧 **Email:** [kentuckyloan@gmail.com](mailto:kentuckyloan@gmail.com) 🌐 **Apply Online:** [www.mylouisvillekentuckymortgage.com](https://www.mylouisvillekentuckymortgage.com) NMLS #57916 | Company NMLS #1738461 *Licensed in Kentucky Only | Equal Housing Lender* *This website is not affiliated with or endorsed by FHA, VA, USDA, KHC, or any government agency. All loan approvals are subject to underwriting guidelines. Not all borrowers will qualify.* --- *Tags: credit score Kentucky mortgage, FHA credit score Kentucky, KHC credit score requirements, improve credit score Kentucky home buyer, Kentucky first time home buyer credit score, minimum credit score Kentucky mortgage loan, USDA credit score Kentucky, VA loan credit score Kentucky, Louisville KY mortgage credit requirements*